There is more than Alternative Investment Funds (AIFs) which have become the most one of the preferred investment vehicles for the high-net-worth individuals (HNIs), family offices, institutional investors, and startups are looking for the well structured capital solutions in India.There are many investors and businesses who are still in doubt to understand the difference between Category I, Category II, and Category III AIFs.

If someone is planning to invest in AIFs, and want to launch an investment fund, or explore emerging AI-driven investment technologies, understanding these categories are very important for making informed financial decisions.

In this guide, we will try to explain everything about Category I, II, and III AIFs in a very simple language — including the structure, benefits, taxation, regulations, examples, and how technology and AI are transforming the AIF ecosystem.

What is an AIF?

There is An Alternative Investment Fund (AIF) is a privately pooled investment vehicle regulated by the Securities and Exchange Board of India (SEBI). The funds used to collect money from the sophisticated investors and invest in assets beyond traditional stocks and bonds.

AIFs generally invest in:

- Startups company

- Private equity

- Venture capital

- Real estate

- Infrastructure development

- Debt instruments

- Hedge funds

AIFs is regulated by the SEBI (Alternative Investment Funds) under the Regulations, 2012.

Types of AIFs in India

The SEBI is classified in AIFs in three categories

- Category I AIF

- Category II AIF

- Category III AIF

Every category has different investment strategies like risk levels, tax implications, and the regulatory benefits.

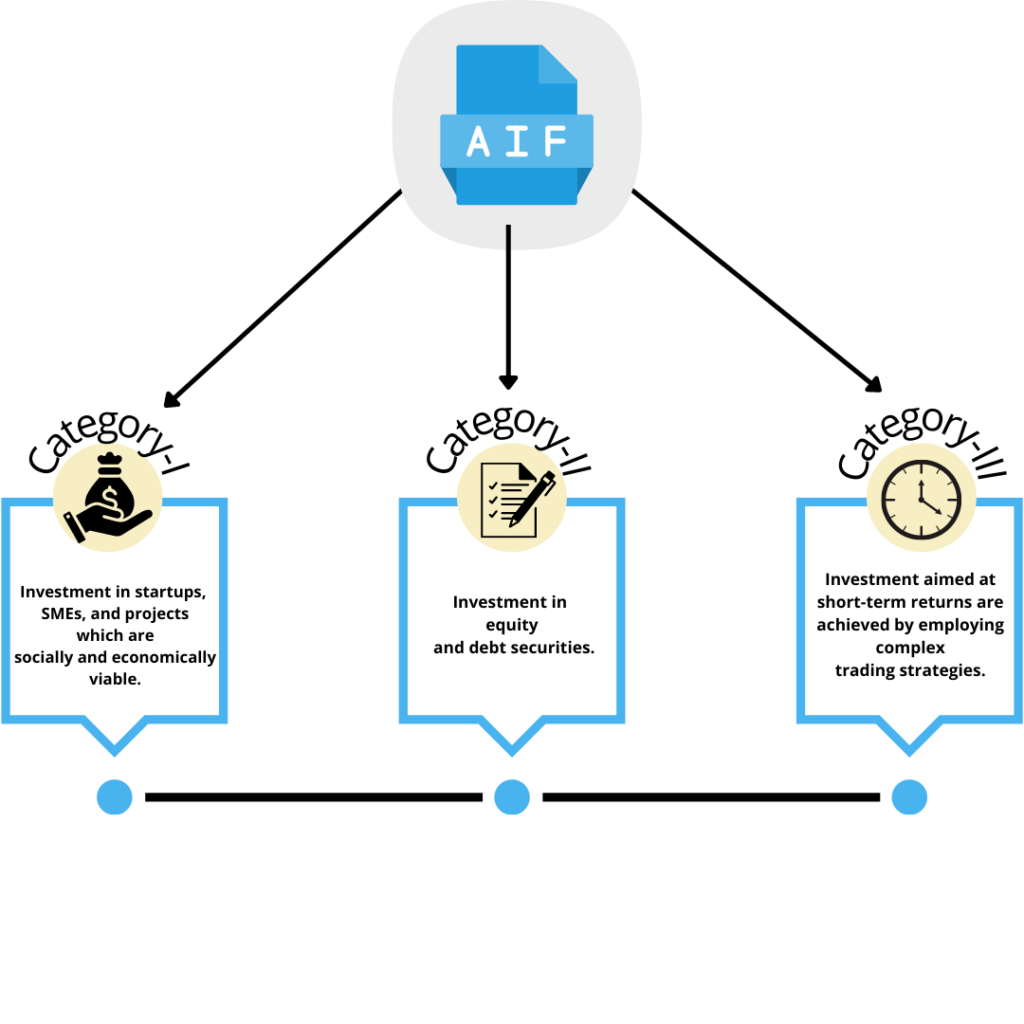

Category I AIF Explained

The Category I AIFs invest in those sectors which are considered socially and economically beneficial for India.

These kinds of funds receive more incentives and support from the government because this sector contribute to economic growth as well as innovation.

Key Features of Category I AIFs

- Invest in the startups in the Newly businesses

- The promotion of the Entrepreuneurship

- Have less investment risk

- Government incentives may apply

- Long-term investment opportunity

Types of Category I AIFs

Venture Capital Funds (VCFs)

Investing in the startups and the high-growth companies.

SME Funds

These are focused in Medium enterprise

Infrastructure Funds

In these Investment in the infrastructure project for example Roads , energy and logistics.

Social Venture Funds

In these the company which creates social welfare gets Funds

Who Should Invest in Category I AIFs?

Category I AIFs are suitable for:

- For the Long-term investors

- Startup-focused investors which can create innovation

- Investors seeking government-supported sectors

- High-risk, high-growth investors

Category II AIF Explained

Category II AIFs are the most common type of AIF in India. These kinds of funds don’t receive incentive through the the government and do not have aggresive trading strategies compare to Category III.

They primarily invest in the private companies, debt instruments, and the unlisted businesses.

Features of Category II AIFs

- There is no leverage expectation for operations.

- Mature business gets investment

- From medium to long term investment

- It is Stable compared to Category III

- Widely used by private equity firms

Different types of Category II AIFs

Private Equity Funds

Private companies which is established gets Investment

Debt Funds

Invest in debt for securities of companies.

Fund of Funds

Invest in other AIFs.

Real Estate Funds

Invest in commercial and residential projects.

Who Should Invest in Category II AIFs?

Ideal for:

- High Net worth individual

- Institutional investors

- Family offices

- Investors seeking balanced risk and return

Category III AIF Explained

In Category III AIFs they use high complex trading strategies and may employ leverage to generate short-term investment returns.

These funds are similar to the hedge funds and actively trade across markets.

Features of Category III AIFs

- Use for leverage and derivatives

- High risk for investment

- Short-term opportunities for trading

- Higher flow of liquidity

- Suitable for sophisticated investors

Examples of Category III AIFs

- Hedge Funds : wide range of assets , debt , real estates

- Quantitative Trading Funds

- AI-powered Algorithmic Trading Funds

- Long-short equity funds

Who Should Invest in Category III AIFs?

Suitable for the :

- Aggressive investors

- HNIs

- Institutional traders

- Investors comfortable with market fluctuations of price

Difference Between Category I, II, and III AIFs

| Feature | Category I AIF | Category II AIF | Category III AIF |

|---|---|---|---|

| Investment Focus on | Startups, SMEs, infrastructure | Private equity, debt | Trading & hedge strategies |

| Government Incentives presence | Yes | No | No |

| Risk Level | Moderate to High | Moderate | Very High |

| Leverage Allowed | Limited | Limited | Yes |

| Investment time period | Long-term | Medium to Long-term | Short-term to Medium-term |

| Liquidity | Low | Moderate | High |

| Type of investor | Growth investors | Balanced investors | Aggressive investors |

| Examples: | Venture capital funds | PE funds | Hedge funds |

Taxation of AIFs in India

Taxation differs depending on the category of the AIF.

Category I and II AIF Taxation

These are categories who generally enjoy pass-through taxation status, meaning income is taxed in the hands of investors rather than the fund itself.

Category III AIF Taxation

Category III do not receive any pass through status and are taxed at their fund level.

Tax regulations can change frequently, so professional tax consultation is advisable.

According to SEBI regulations:

- Minimum investment should be 1 crore rupee for the investor.

- And For the directors/employees/managers of the fund should be 25 lakhs.

These are mainly designed for sophisticated investors.

Benefits of Investing in AIFs

Portfolio Diversification

In AIFs we explore beyond traditional equity and also for the debt markets.

Access to High-Growth Opportunities

Investors can directly participate in startups, private companies, and emerging sectors for the high return.

Fund Management by professional

It is Managed by experienced professionals and investment experts to reduced the risk and uncertainties of your funds.

Potential for Higher Returns

Alternative assets can be generated higher returns compare to conventional investments.

Risks Associated with AIFs

AIFs offer strong growth potential, they also come with high risks:

- Limited liquidity

- Market uncertainty

- Government Regulation

- High minimum investment

- Complex structures

Investors should evaluate their risk appetite more carefully before investment in company.

How AI is Transforming the AIF Industry

Artificial Intelligence is changing very fast the way Alternative Investment Funds operate.

Modern AIF firms are using AI for:

- Portfolio optimization

- For identifying the risk

- Detection of funds

- Predictive analytics

- Algorithmic trading

- Investor reporting automation

AI agents can process a huge financial datasets in real-time, helping the fund managers make faster decision and more reliable investment decisions.

Businesses looking to integrate intelligent automation into investment operations can leverage custom AI solutions from Winklix AI Agent Development Services. Their AI-driven systems help enterprises build autonomous AI agents for finance, investment management, and operational automation.

Why Understanding AIF Categories Matters

Choosing the right AIF category depends on several factors:

- Investment goals

- Risk tolerance

- Liquidity requirements

- Tax planning

- Investment horizon

A startup-focused investor may prefer Category I, while a stable private equity investor may choose Category II. Aggressive investors looking for high-frequency strategies may opt for Category III.

Understanding these differences helps investors make smarter financial decisions.

Future of AIFs in India

India’s alternative investment market is expected to grow further in future due to significantly aspects:

- Rising the ecosystem

- Due to Increased HNI participation

- The growth of the private capital

- AI-driven investment management

- Increase of fintech and wealthtech platforms

As the financial technology is evolving, AI -powered fund management and automation is likely to become more in future of AIFs .

Final Thoughts

Alternative Investment Funds are reshaping India’s investment landscape by offering sophisticated investors access to private markets, startups, and advanced trading opportunities.

The understanding of difference between Category I, II, and III AIFs is very important key aspects before making any investment decisions. Each and every category serves different investor needs, risk profiles, and financial goals.

As AI automate and continue to transform financial services, the future of AIF management will become more increasingly data-driven and intelligent. Businesses and investment firms are adopting AI-powered solutions early will gain a strong competitive advantage in the evolving alternative investment ecosystem.

Frequently Asked Questions (FAQs)

Category I focuses on startups and socially beneficial sectors, Category II focuses on private investment and debt investments, while Category III invest in complex trading and hedge fund strategies.

The category II AIFs are find safe and considered relatively stable for the investment.Category III is avoided because of leverage trading strategies .

Yes, Category III AIFs are allowed to use leverage and derivatives for investment strategies.

The minimum investment amount is generally ₹1 Crore per investor.

Yes, AIFs are regulated by the (SEBI)Securities and Exchange Board of India

The Category I AIFs primary focus on investment in startups, SMEs, and innovative driven businesses.

AI helps in many aspects like prediction analytics, algorithmic trading, investor analytics, portfolio management, and automation of investment operations.

AIFs offer access to alternative assets and potentially higher returns, but they also comes with the higher barrier risk and it take larger investments compared to mutual funds.