For decades, stock markets and mutual funds have dominated the portfolios of Indian investors. But as wealth creation accelerates and new-age wealth holders become more sophisticated, they are seeking opportunities that go beyond traditional equities. Enter Alternative Investment Funds (AIFs)—a growing asset class that is redefining the way affluent investors diversify, manage risk, and capture long-term growth.

Why Investors Are Moving Beyond Stocks

New-age wealth holders are no longer satisfied with standard market-linked returns. With access to global trends, evolving risk appetites, and higher net worth levels, they are increasingly seeking alternative avenues. Some key reasons for this shift include:

- Diversification: Reducing overexposure to volatile equity markets.

- Specialized Strategies: Access to private equity, venture capital, hedge funds, real estate, and infrastructure investments.

- Long-Term Growth: Potential for higher alpha compared to traditional stocks.

- Professional Management: AIFs are regulated, structured, and managed by expert fund managers.

The Growing Relevance of AIFs in India

In India, AIFs are regulated by SEBI, ensuring transparency and investor protection. They cater to high-net-worth individuals (HNIs) and institutional investors looking for niche opportunities. The popularity of AIFs has surged in recent years, particularly among millennials and Gen-Z entrepreneurs who understand the importance of diversification beyond listed securities.

According to industry reports, the AIF industry in India has witnessed double-digit growth, fueled by rising investor demand and innovative fund strategies. From real estate-focused funds to venture capital supporting start-ups, AIFs are offering wealth holders opportunities previously reserved for ultra-elite investors.

Navigating AIF Registration: What Investors and Fund Managers Need to Know

For fund managers and institutions aiming to establish an AIF, Alternative Investment Fund Registration in India is a crucial compliance step. SEBI mandates specific registration processes to ensure transparency and protect investor interests.

Today, the process has become more streamlined with the availability of Online AIF Registration in India. Fund managers can now apply for AIF Registration Online in India, making the process faster, more efficient, and aligned with India’s digital compliance ecosystem.

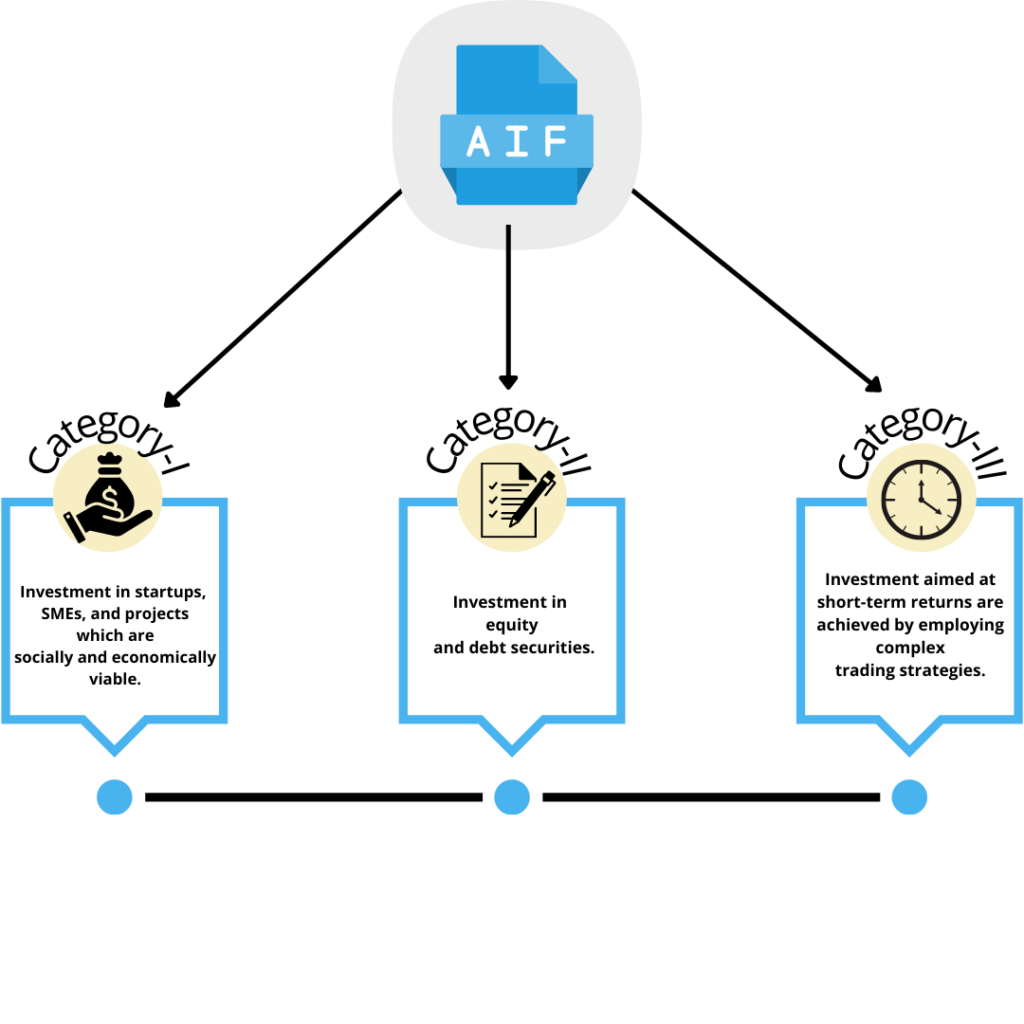

Whether it’s a Category I, II, or III AIF, understanding the legal and regulatory framework is essential. Many institutions rely on an AIF Registration Consultant to navigate the complexities, ensure proper documentation, and achieve faster approvals.

Online Alternative Investment Fund Registration in India: The Way Forward

With the growing appetite for alternatives, regulatory clarity, and simplified Online Alternative Investment Fund Registration in India, the AIF market is poised for exponential growth. More and more new-age wealth holders are realizing that AIFs can be the bridge between conventional investments and innovative wealth-building strategies.

Conclusion

As India’s wealth landscape evolves, AIFs are emerging as a critical investment vehicle for those who wish to diversify beyond stocks. For fund managers, efficient AIF Registration Online in India ensures credibility, compliance, and faster market entry. For investors, AIFs represent a gateway to sophisticated wealth creation strategies that align with global best practices.

In short, AIFs are not just a trend—they are the future of wealth management in India.