Introduction

India’s alternative investment fund market is grown significantly over the last few decades , making Alternative Investment Funds (AIFs) is one of the most preferred investment for the private firms, ventures, hedge funds and the institutional investors. To operate this legally in India, this AIF must contain registration from the Securities and Exchange Board of India (SEBI) SEBI (Alternative Investment Funds) Regulations, under 2012.

If you want plan for launching an investment fund in India, the understanding of AIF registration process is most important element for understanding AIF. This guide explains each step by step in detail.

What is an Alternative Investment Fund (AIF)?

An Alternative Investment Fund (AIF) is a specialized investment vehicle that pools capital from multiple investors to invest in non-traditional asset classes, such as private equity, real estate, hedge funds, venture capital, and commodities. These funds are typically managed by professional fund managers and are structured as limited partnerships or limited liability companies.

AIFs can be structured as:

- Trusts

- Limited Liability Partnerships (LLPs)

- Companies

- Body Corporates

These are the funds which are regulated by SEBI and are generally used for the investments in startups, private companies, infrastructure projects, real estate, private equity, venture capital, debt instruments, and hedge fund strategies.

Categories of AIFs in India

Before starting any registration process the fund managers has to choose the appropriate AIF category according to need.

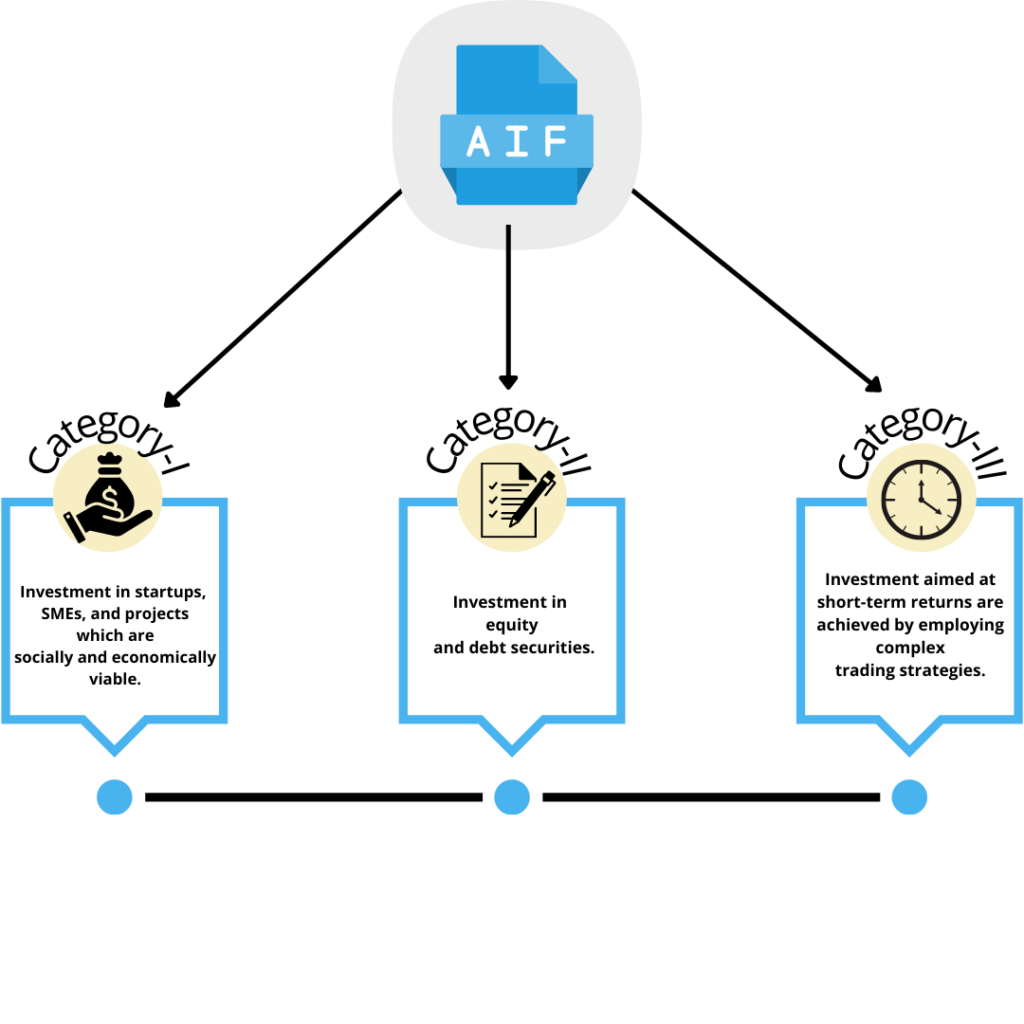

Category I AIF

These are AIFs that invest on start up and early stage venture , small and medium enterprises , infrastructure . AIFs I also Include investment in social and economically desire group. Category I considered to have moderate risk and low regulatory restriction compare to other AIFs categories.

Examples:

- Venture Capital Funds

- Angel Funds

- Infrastructure Funds

- SME Funds

- Social Venture Funds

Category II AIF

These are AIFs that do not fall under both categories AIFs I and AIFs II . This category known for moderate risk and uncertainites for investment . These category include private Equity funds , debt funds , and funds invest in real state among India.

Examples:

- Private Equity Funds

- Debt Funds

- Fund of Funds

Category III AIF

Category III Use complex stragies for These are AIFs that use complex trading strategies and leverage to generate high returns for investors, such as hedge funds, among others.

Step-by-Step AIF Registration Process in India

Step 1: Determine the Fund Structure

The first step is decide the legal structure of the fund for investment process.

And determining whether the funds fall in which category either is category I , II, Or III . Choosing the correct category is critical because regulatory requirements differ for each category.

You must:

- Create the trust, LLP, or company

- Draft constitutional documents

- Obtain PAN and other registrations

- Establish the investment management entity

SEBI reviews the legal structure carefully before granting approval.

Step 2: Select the Appropriate AIF Category

The second step is to determine whether the the fund falls under which is it Category I, Category II, or Category III.

The category affects investment restrictions, compliance requirements, and operational guidelines. Selecting the correct category at the beginning helps avoid regulatory complications later.

Step 3: Appoint the Sponsor and Investment Manager

Every AIF requires a sponsor and an investment manager for the analyising of funds.

The sponsor establishes the fund and contributes the required continuing interest, while the investment manager is responsible for managing investments and making portfolio decisions.

SEBI reviews the qualifications, experience, and regulatory track record of these entities during the registration process.

Step 4: Draft the Private Placement Memorandum (PPM)

The Private Placement Memorandum (PPM) is one of the most important documents for the AIF registration in India.

It contains key information such as:

- Investment strategy for the investors

- Risk factors and uncertainty

- Governance structure

- Fee structure

- Investor rights

- Exit mechanisms

A well-drafted PPM improves transparency and increases the likelihood of regulatory approval.

Step 5: Prepare Documentation

The Applicants must have all the documents which are needed for the investment before filing the application.

Common documents include:

- Trust Deed or LLP Agreement

- Certificate of Incorporation

- PAN card details

- Bank account details

- Sponsor information

- Investment manager details

- Financial statements

- Compliance declarations

- Private Placement Memorandum

Accurate documentation helps prevent delays during SEBI review.

Step 6: Submit the Application to SEBI

This is one of the most important key element of the AIFs registration because application is officially submitted and the review as well as approval will be done SEBI. The application for AIF registration is submitted through SEBI’s online intermediary portal. The document should well prepared for the delay of registration.

The applicant must complete Form A, upload supporting documents, and pay the applicable fees.

Once submitted, SEBI begins its review process.

Step 7: Respond to SEBI Queries

Before the approval the SEBI may seek clarifications regarding the fund structure, investment strategy, governance framework, or the documentation.

Timely and accurate responses are essential for smooth approval.

Step 7: Respond to SEBI Queries

These is the final step SEBI will ask for the document clarification regarding several step for the investment. Respond to SEBI Queries objective is to ensure that the proposed Alternative Investment Fund complies with all regulatory requirements and adequately protects investor interests. In these several Queries may ask :

Asking for the missing documents , clarification regarding the fund structure, Investors protection, Governance and compliance framework concern.

How Long Does AIF Registration Take?

The time taken for AIF registration process depends on the situation of complexity of the application and the quality of documentation that has been submitted.

In most cases:

- Fund Structuring: 2–4 Weeks

- Documentation Preparation: 3–6 Weeks

- SEBI Review: 4–12 Weeks

- Final Approval: 2–4 Weeks

Most AIF registrations are completed within 2 to 8 months.

Conclusion

AIFs is very important crucial step for every fund manager , venture capital funds ,private equity funds and investment professionals looking to establish a regulated investment platform in India. By selecting the best AIFs category , fund structure , preparing all the documents and analysing the document which is needed for the AIFs registration process. By selecting the appropriate fund structure, preparing robust documentation, drafting a comprehensive PPM, and complying with SEBI regulations, applicants can successfully launch and operate an Alternative Investment Fund.

Frequently Asked Questions (FAQs)

An Alternative Investment Fund that has registered with the Securities and Exchange Board of India (SEBI) is known as a SEBI AIF Registration. AIFs are investment vehicles that invest in assets such as private equity, venture capital, real estate, and debt securities.

All the registration process are done and approval from the SEBI is most important . In these approval from SEBI to establish and operate an Alternative Investment Fund in India.

Yes, it is very important in every Alternative investment funds, and must be register with SEBI.

A Trust, LLP, Company, or Body Corporate can apply for AIF registration subject to SEBI regulations.

It takes almost 2-8 months according to document submission to SEBI. If any document is not missing it will approve soon.

A PPM is a legal document that outlines the fund’s investment strategy, risks, fee structure, governance, and investor rights.

AIF registration provides regulatory recognition, investor confidence, fundraising opportunities, and a structured framework for managing investments.