500000+

Happy Customers

Funding in NBFC Advisory Services

Professional support for NBFC fundraising, bank finance, FDI, private equity, commercial paper, bonds, securitization and asset-liability planning.

NBFCs, or Non-Banking Financial Companies, play a crucial role in India's financial ecosystem by offering credit and financial services outside the traditional banking structure. Unlike banks, NBFCs are not permitted to accept demand deposits such as CASA deposits, which are usually a low-cost source of funds for banks.

Due to this limitation, NBFCs depend on alternative funding sources to support their lending operations, business expansion and liquidity requirements. Since these funds are often raised at a higher cost, NBFCs must carefully manage their borrowing structure, interest margins, repayment cycles and overall risk exposure.

For any RBI-registered NBFC startup, fundraising is essential to support business operations, lending capacity, technology development and market expansion. Venture funding becomes especially important for NBFCs that use digital platforms, data-driven underwriting, automation and strong risk management practices to scale their business.

Venture capital and startup funding help NBFCs build a stronger capital base, expand their customer reach and invest in better credit assessment systems. Since growth in the NBFC sector requires continuous capital deployment, fundraising should be treated as an ongoing strategic activity rather than a one-time requirement.

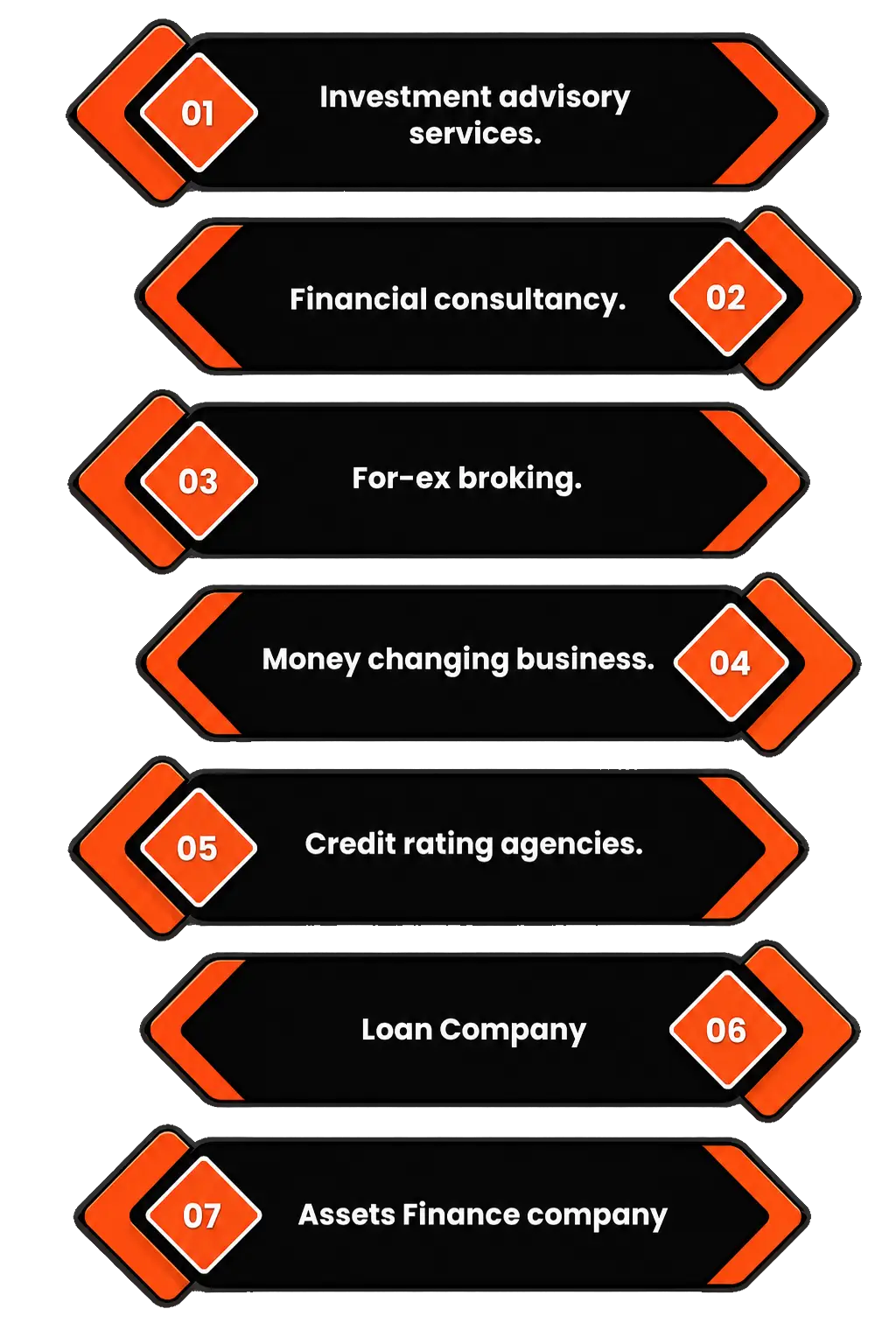

Banks may provide working capital loans, term loans and other credit facilities to RBI-registered NBFCs. Such funding can be used to support lending activities, liquidity needs, portfolio growth and business expansion, subject to the NBFC's financial strength, compliance status, creditworthiness and repayment capacity.

Private equity and venture capital firms actively invest in NBFCs with scalable business models, strong compliance systems and technology-led lending processes. These investors provide capital to support growth, improve operational efficiency, strengthen risk management and expand the NBFC's presence in India's financial services market.

Non-Banking Financial Companies can raise funds through multiple domestic and international sources. The right funding option depends on the NBFC's size, credit rating, asset quality, regulatory compliance, liquidity position and long-term business plan.

Once an NBFC builds a strong asset base and demonstrates stable business performance, it may approach banks and financial institutions for long-term loans. These loans can be secured or unsecured and may follow a structured repayment schedule or bullet repayment model. A strong credit rating, healthy portfolio quality and sound repayment capacity help NBFCs access larger capital at more competitive rates.

Foreign Direct Investment is an important funding route for eligible NBFCs. Subject to applicable FDI policy, RBI regulations, FEMA provisions and sector-specific conditions, foreign investment may be permitted up to 100% under the automatic route for eligible financial services activities.

Commercial paper is a short-term unsecured money market instrument that eligible NBFCs may issue to raise working capital or meet short-term liquidity requirements. It is generally used by financially sound companies with strong credit ratings and is issued in accordance with applicable RBI and market regulations.

NBFCs may raise funds by issuing bonds, non-convertible debentures or other debt instruments to investors. The coupon rate, maturity period and repayment structure are usually determined by the NBFC's credit rating, financial position, market conditions and investor appetite. Bond issuance can support long-term liquidity planning and portfolio expansion.

Loan securitization allows NBFCs to convert existing loan portfolios into marketable securities and raise funds from investors. This method is commonly used by NBFCs and Housing Finance Companies to improve liquidity, manage asset-liability mismatches and free up capital for fresh lending.

Effective fundraising in an NBFC requires a clear assessment of liquidity needs, borrowing costs, repayment obligations and asset-liability alignment. The following points should be considered while evaluating a fundraising strategy:

The rupee resources department is responsible for planning and raising funds through short-term and long-term instruments. It ensures that the NBFC has adequate liquidity to meet lending and operational requirements. The treasury department manages fund deployment, liquidity planning, asset-liability variations and money market instruments after funds are raised and received by the company.

Treasury and rupee resources teams rely on key risk indicators to manage asset-liability matching, funding decisions, liquidity gaps, interest-rate exposure and overall financial stability.

Liquidity risk arises when an NBFC is unable to meet its financial obligations on time or cannot sell assets quickly without incurring significant losses. Proper liquidity planning helps ensure that repayment commitments and lending operations continue smoothly.

Interest rate risk occurs when changes in market interest rates affect the NBFC's borrowing cost, lending income, net interest margin or overall profitability. Managing this risk is essential for protecting earnings and maintaining balance sheet stability.

Foreign exchange risk may arise when an NBFC has exposure to foreign currency borrowings, investments or transactions. Adverse currency movements can result in financial losses, especially when open positions are not properly hedged.

Equity price risk refers to the possibility of losses due to fluctuations in the value of equity investments held by an NBFC. These investments may include listed shares, private equity holdings or other market-linked instruments. NBFCs should assess such risks carefully and ensure that investment decisions follow proper approval and monitoring systems.

Market interest-rate movements may also affect the economic value of an NBFC's balance sheet. Since NBFCs usually manage diverse loan products and borrowing structures, it is important to measure interest-rate risk on the banking book. Treasury teams may assess maturity gaps, repricing gaps and duration gaps to understand the possible impact on earnings and economic value.

The Asset Liability Committee, or ALCO, plays an important role in managing liquidity risk, interest-rate risk and balance sheet stability within an NBFC. The committee is usually led by senior management and CXOs who monitor borrowing costs, liquidity gaps, profitability pressure and funding strategy, especially during volatile or challenging market conditions.

Get in touch with the BIATConsultant team to discuss your NBFC funding requirements, business structure and eligibility. The initial consultation usually takes around 20 to 25 minutes.

After understanding your requirements, we assign a dedicated account manager to guide you through the entire process. Our team helps you evaluate suitable funding options, documentation requirements and compliance steps.

Stay updated at every stage of your application through regular team updates and process tracking. This helps you monitor the progress of documentation, submission and funding-related formalities.

Once the process is completed, you will receive the required documents, confirmations and deliverables through email or physical delivery, depending on the nature of the service.

Funding in NBFC refers to the process through which a Non-Banking Financial Company raises capital for lending operations, liquidity management, portfolio growth and business expansion through sources such as bank loans, private equity, FDI, bonds, commercial paper and securitization.